Global money laundering is estimated to account for 2% to 5% of global GDP each year, with much of it remaining undetected. At the same time, traditional anti-money laundering (AML) systems are struggling to keep pace. Legacy, rules-based solutions often generate overwhelming volumes of false positives, increasing compliance costs while making it harder for teams to identify genuine financial crime.

As regulatory expectations evolve, technology is reshaping how anti money laundering checks are performed. Artificial intelligence (AI), machine learning, automation, and real-time analytics are enabling faster, more accurate customer due diligence, transaction monitoring, and sanctions screening. For organizations operating across high-risk and cross-border markets, adopting these technologies is becoming essential to strengthening compliance, improving operational efficiency, and managing financial crime risk.

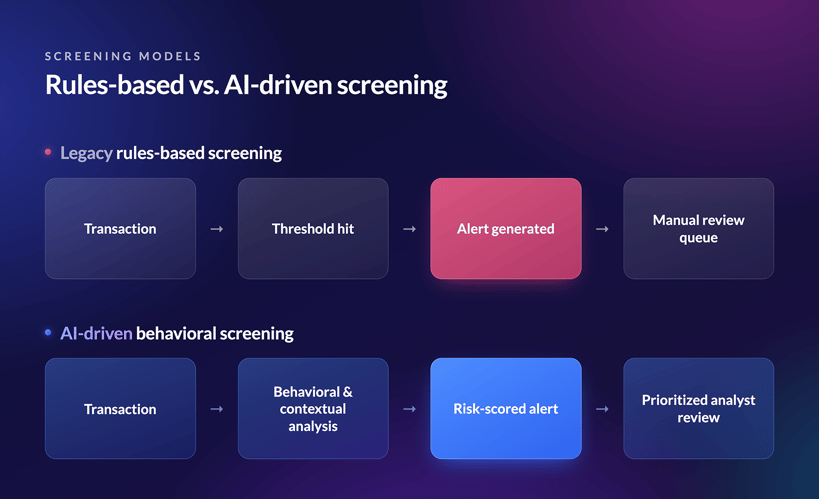

The Limits of Legacy AML Screening

Traditional AML systems were built around static thresholds: fixed transaction amounts, fixed velocity limits, and rule sets that flag activity matching a predefined pattern. These systems were adequate when laundering typologies were relatively stable and transaction volumes were manageable by human review teams. Neither condition holds today. Digital payments, cross-border e-commerce, and increasingly complex corporate ownership structures have multiplied both the volume and the sophistication of transactions that compliance teams must assess.

The consequence is a system under strain from two directions. On one side, static rules cannot adapt quickly enough to new laundering methods — structuring, mule networks, trade-based laundering through invoice manipulation, and the use of shell entities across multiple jurisdictions. On the other, the sheer volume of low-quality alerts generated by rigid thresholds buries the alerts that matter. Analysts spend most of their time clearing noise rather than investigating substantive risk, which is precisely the dynamic that has pushed AI adoption from an innovation project to what many institutions now treat as an operational necessity.

How AI and Machine Learning Are Reshaping Transaction Monitoring

The core change underway is a move from fixed-threshold alerting to behavioural, contextual risk scoring. Rather than flagging a transaction because it crosses a static dollar amount, AI-driven monitoring evaluates a customer's transaction history, typical behaviour patterns, and surrounding context — location, counterparty risk, sector norms — to assess whether an individual transaction is genuinely anomalous for that specific customer. This behavioural approach allows institutions to identify suspicious activity with greater precision while reducing the volume of alerts that do not warrant investigation.

Several capabilities are driving this shift in practice:

Real-time behavioural analytics:

Modern monitoring platforms assess transactions as they occur rather than through periodic batch review, allowing institutions to flag and, where necessary, interdict suspicious activity before funds move further through the financial system.

Machine-learning-enabled sanctions and PEP screening:

Fuzzy-matching algorithms now reduce false positives in name-screening against sanctions and politically exposed persons lists, a persistent source of alert fatigue in cross-border compliance teams working with transliterated names across Arabic, French, and English-language jurisdictions.

Agentic AI for first-level triage:

A newer generation of tools automates the initial stages of alert investigation — gathering supporting data, applying consistent risk logic, and preparing case files — so that human analysts focus their time on alerts that genuinely warrant judgment.

Generative AI for documentation:

Compliance teams are beginning to use generative AI to draft Suspicious Activity Reports and supporting regulatory correspondence, reducing the administrative burden that has historically diverted analyst time away from investigation.

Digital identity and biometric verification:

Automated document, biometric, and liveness checks are compressing onboarding timelines while addressing deepfake and synthetic-identity risks that traditional document review was never designed to catch.

.png?width=880&height=500&name=img%20comparison%202%20(1).png)

What Regulators Are Saying

Technology adoption in AML is not occurring in a regulatory vacuum. The FATF has actively encouraged the responsible use of new technologies through its Digital Transformation of AML/CFT program, which examines how financial institutions, financial intelligence units, and law enforcement agencies can deploy AI, machine learning, and big data analytics without compromising the integrity of the compliance function. FATF's most recent horizon-scanning work on AI, published in late 2025, takes a more cautious tone: it maps both the opportunities AI creates for detection and the emerging risks — including AI-generated deepfakes — that criminals themselves are beginning to deploy against verification systems.

This dual framing matters for how institutions should read the AI-in-AML narrative. Regulators are not simply endorsing automation; they are conditioning that endorsement on explainability, auditability, and continued human oversight of high-stakes decisions. Any AI-driven risk model that cannot be explained to an examiner, or that operates as a black box in a suspicious activity determination, creates a new category of regulatory risk even as it solves an old one. For compliance functions, this means technology procurement decisions increasingly hinge on a vendor's ability to document model logic and decision rationale, not simply on detection accuracy in isolation.

Why This Matters More in the Middle East and Africa

Regional dynamics add urgency to this shift. The Basel AML Index 2025 recorded a small increase in average money laundering risk across the Middle East and North Africa, even as several Sub-Saharan African countries — including Nigeria, South Africa, Tanzania, Mozambique, Mali, and Burkina Faso — exited the FATF grey list during the same period, reflecting genuine reform progress. That divergence illustrates a broader pattern across the region: improvement is real but uneven, and institutions operating across multiple MEA jurisdictions face a compliance landscape where risk profiles can shift meaningfully from one country, or one supervisory cycle, to the next.

Technology adoption is proceeding unevenly as well. The Middle East and Africa accounted for roughly $1.78 billion of the global RegTech market in 2025 — a relatively modest share of the global total, but one projected to keep expanding as regional banks and fintechs face the same cross-border payment complexity and sanctions-exposure risk as their counterparts in more mature markets. For institutions doing business with counterparties across francophone West Africa, the Gulf, and North Africa simultaneously, AI-enabled screening that can handle multilingual name variants, informal corporate structures, and rapidly changing sanctions designations is no longer a competitive advantage — it is close to a baseline operating requirement.

Practical Implications for Compliance and Risk Teams

The overarching lesson for compliance officers and risk managers is straightforward: AI is genuinely improving AML detection, but its effectiveness is conditional, not automatic. A model is only as good as three things sitting underneath it — transparency in how it reaches a decision, the quality of the data it is trained and run on, and the reliability of the corporate ownership, sanctions, and adverse-media information it screens against. Strip away any one of those, and even the most sophisticated model will underperform or, worse, produce confident-looking results that do not hold up to examiner scrutiny.

This is where the AI-in-AML narrative tends to oversimplify, particularly for institutions operating across the Middle East and Africa. A model trained primarily on data patterns from mature, high-transparency markets does not automatically translate into reliable risk detection in jurisdictions where corporate registries are incomplete, beneficial ownership disclosure is inconsistent, and entity names carry multiple valid transliterations across Arabic, French, and English. In these environments, an AI system is only as sharp as the underlying entity data feeding it — and that data gap is a regional and structural one, not something a better algorithm alone can close.

Closing it requires local market knowledge: verified corporate registry data, accurately resolved beneficial ownership structures, and sanctions and adverse-media screening built to handle the naming conventions and disclosure gaps specific to MEA jurisdictions. This is precisely the layer that regional business intelligence providers with deep, on-the-ground coverage of Middle East and African markets — firms like Cedar Rose — are built to supply, working alongside AI-driven monitoring rather than in place of it. The institutions that pair strong AI capability with that kind of verified, regionally grounded data are the ones best positioned to make automated compliance decisions that actually withstand regulatory review.

Conclusion

The transformation of anti-money laundering checks is not a single technology upgrade but a structural change in how financial institutions approach detection, investigation, and reporting. AI-driven transaction monitoring, automated identity verification, and machine-learning risk scoring are replacing static, rules-based screening because the volume and sophistication of financial crime has outgrown what manual processes can handle. Regulators, led by FATF, have broadly endorsed this direction while insisting that explainability and human judgment remain central to any AI-enabled compliance program. For institutions operating across the Middle East and Africa, where regional risk profiles are shifting unevenly and RegTech adoption still lags more mature markets, the practical priority is straightforward: modernize detection capability without compromising the underlying data quality and human oversight that make any automated system defensible to a regulator. The institutions that get this balance right will be better positioned for correspondent banking relationships, cross-border expansion, and investor confidence in the years ahead.

Sources & References:

- United Nations Office on Drugs and Crime (UNODC) – Money-Laundering Overview: https://www.unodc.org/unodc/en/money-laundering/overview.html

- Financial Action Task Force (FATF) – Opportunities and Challenges of New Technologies for AML/CFT: https://www.fatf-gafi.org/en/publications/Digitaltransformation/Opportunities-challenges-new-technologies-for-aml-cft.html

- Financial Action Task Force (FATF) – Horizon Scan: AI and Deepfakes (2025): https://www.fatf-gafi.org/en/publications/Methodsandtrends/horizon-scan-ai-deepfake.html

- Basel Institute on Governance – Basel AML Index 2025, 14th Public Edition: https://baselgovernance.org/publications/basel-aml-index-2025

- Basel Institute on Governance / Mo Ibrahim Foundation – Basel AML Index: Progress in Africa (2025): https://mo.ibrahim.foundation/news/2025/basel-aml-index-shows-progress-fight-against-financial-crime-africa

- Fortune Business Insights – RegTech Market Size Report (2025–2026 figures, including MEA segment): https://www.fortunebusinessinsights.com/regtech-market-108305

- fintech.global – Why AI Is Becoming Essential for AML in 2026 (Wipro false-positive research cited): https://fintech.global/2026/01/14/why-ai-is-becoming-essential-for-aml-in-2026/

.png?width=352&name=website%20img%20(1).png)